Mua tiền điện tử

thẻ

Giao dịch P2P

Mua USDT trên thị trường

Thẻ Credit/Debit

Mua tiền mã hóa bằng thẻ Visa hoặc MasterCard

Dịch vụ thanh toán của bên thứ ba

Mua tiền mã hóa qua MoonPay, Simplex và nhiều dịch vụ khác

BitMart Card

Giúp bạn sống theo phong cách tiền mã hóa

Thẻ trả trước tiền mã hóa

Nhận thẻ Mastercard có thể sử dụng ngay

USDⓈ-M

Sử dụng USDⓈ làm tài sản đảm bảo

COIN-M

Sử dụng chính COIN làm tài sản đảm bảo

TradFi

Dịch vụ giao dịch trọn gói cho kim loại, cổ phiếu và ngoại hối

Giao dịch demo

Tìm hiểu cách giao dịch không gặp rủi ro

Tổng quan về Futures

Nền tảng toàn diện cho Futures

Futures King

Quỹ thưởng 478,000 USDT

Tăng trưởng

Rewards

Rút thăm Futures hàng ngày

100% cơ hội chiến thắng với giao dịch hàng ngày

Rút thăm Spot hàng ngày

Nhận các giải thưởng lớn trị giá 8,888 USDT

Nạp tiền điện thoại

Nạp tiền điện thoại di động dễ dàng, online, bảo mật

Send

Send money globally, fast and secure

BitMart Mall

Trực tiếp trên tiền mã hóa

GMX Dữ liệu giá trực tiếp

Giá GMX hôm nay là $ 5.94 (GMX/USD). Với vốn hóa thị trường là $ 62.01M USD. Khối lượng giao dịch 24 giờ là $ 92,518.96 USD, Biến động giá trong 24 giờ là -0.50%, Và lượng cung lưu hành là 10.43M GMX.

GMX GMX Lịch sử giá USD

Theo dõi giá của GMX hôm nay, 7 ngày, 30 ngày và 90 ngày

Kỳ

Thay đổi

Biến động (%)

Hôm nay

$ 0.039

-0.67%

7ngày

$ 0.55

10.41%

30ngày

$ 0.71

13.79%

90ngày

$ 0.14

-2.46%

Sở hữu GMX ngay

Mua và bán GMX dễ dàng và an toàn trên BitMart.

GMX Thông tin thị trường

$ 5.82 Biến động 24 giờ $ 5.97

Cao nhất từng ghi nhận

$ 91.21

Thấp nhất từng ghi nhận

$ 3.79

Biến động 24 giờ

-0.50%

Khối lượng 24 giờ

$ 92,518.96

Nguồn cung lưu hành

10.43M

GMX

Vốn hóa thị trường

$ 62.01M

Nguồn cung tối đa

13.25M

GMX

Vốn hóa thị trường đã pha loãng hoàn toàn

$ 78.77M

Giao dịch GMX

GMX X Insight

𝕯𝖆𝖓𝖌𝖊𝖗

OnChain_Analyst

Researcher

C

52.1K @safetyth1rd

52.1K @safetyth1rd Tăng giá

The tweet analyzes the perpetual contract DEX market and recommends six data-driven platforms worth watching.

Today in DeFi D

17.3K @todayindefi Some protocols are generating $5B volume weekly while having no token.

6 perps dexes worth looking into - ranked by volume + TVL, not vibes.

Full guide:

https://t.co/LkuplbdTjX https://t.co/rq0I9xUyje

2

2

1

1

809

809

2026-07-03 14:57

Xu hướng của GMX sau khi phát hành

Tăng giá

The tweet analyzes the perpetual contract DEX market and recommends six data-driven platforms worth watching.

SatoshiCrypt BITUNIX

Trader

Influencer

C

52.5K @SatoshiBitunix Tăng giá

Suggest traders be patient and trade smartly, not chase the market, to achieve profit.

SatoshiCrypt BITUNIX

Trader

Influencer

C

52.5K @SatoshiBitunix GM Crypto X

GM Bitunix Fam 💚

I stopped trying to trade every move

Ironically

That’s when I started making more money.

Sometimes the highest-paying trade

Is the one you don’t take

This could be the trade

The week

Or the opportunity you’ve been waiting for

But only if you’re patient enough to let it come to you

Don’t chase the market

Make the market come to you

53

30

6.5K

53

30

6.5K

2026-07-03 07:27

Xu hướng của GMX sau khi phát hành

Tăng giá

Suggest traders be patient and trade smartly, not chase the market, to achieve profit.

Specter

OnChain_Analyst

Security_Expert

S

13.7K @SpecterAnalyst Cực kỳ bi quan

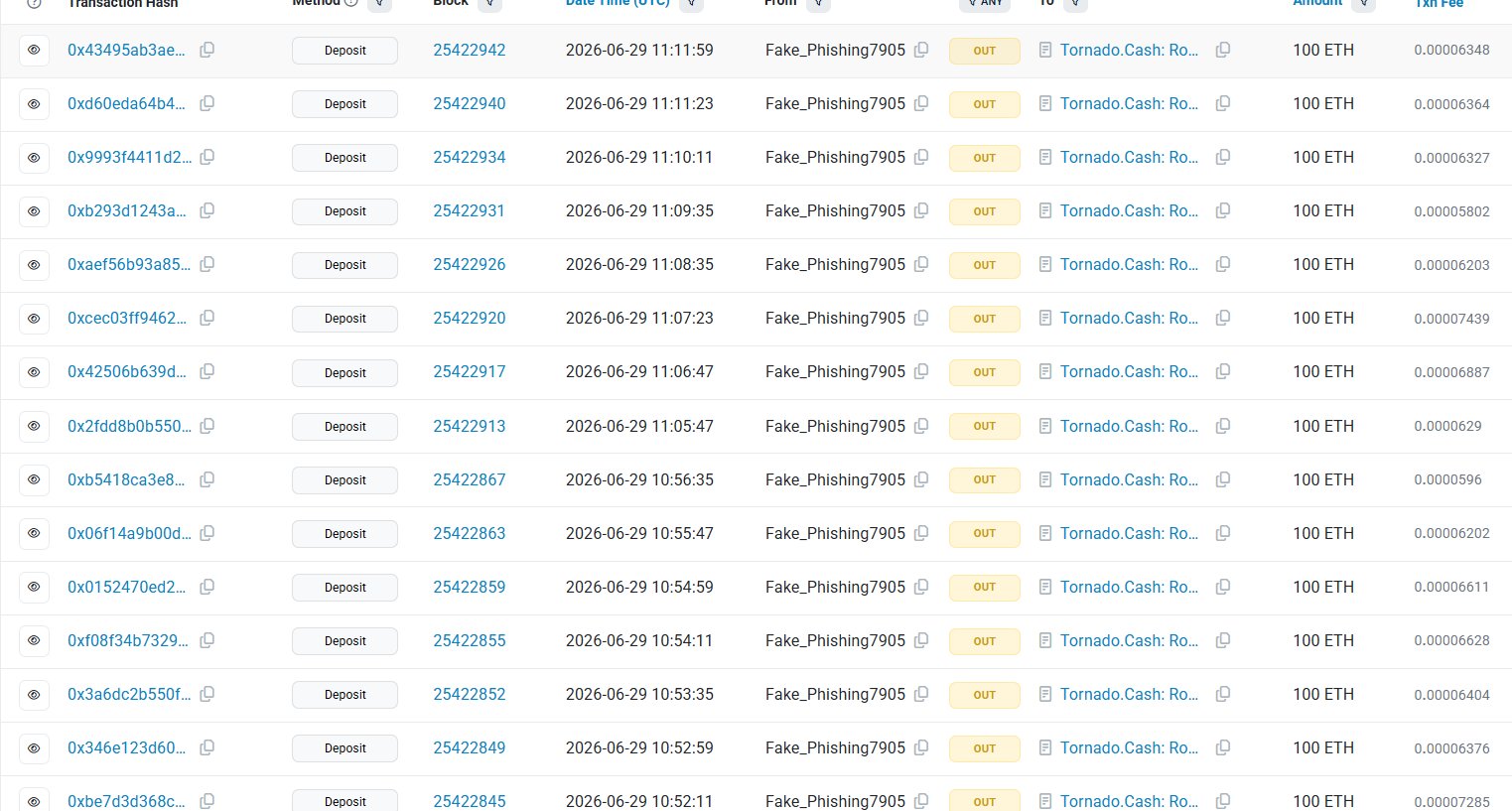

The hacker swapped GMX for ETH and then deposited it in batches into Tornado Cash for laundering, with fund movements after three years of inactivity.

Specter

OnChain_Analyst

Security_Expert

S

13.7K @SpecterAnalyst The attacker has finally begun laundering the stolen funds after more than three years of inactivity.

In January 2023, the attacker swapped the stolen GMX for 2,819 ETH, worth $3.4M at the time. Due to ETH's price appreciation, those funds are now worth $4.4M.

The assets remained dormant until a few minutes ago, when the attacker deposited the stolen ETH into Tornado Cash in 28 of 100 ETH each.

Stay smart.

57

4

10.5K

57

4

10.5K

2026-06-29 18:57

Xu hướng của GMX sau khi phát hành

Giảm giá

The hacker swapped GMX for ETH and then deposited it in batches into Tornado Cash for laundering, with fund movements after three years of inactivity.

Dự đoán giá

Thời điểm phù hợp để mua GMX là khi nào? Liệu tôi nên mua hay bán GMX bây giờ?

Khi quyết định xem đây có phải là thời điểm tốt để mua hoặc bán GMX (GMX) hay không, điều quan trọng trước tiên là phải phù hợp với chiến lược giao dịch và mức độ chấp nhận rủi ro của riêng bạn. Các nhà đầu tư dài hạn và các nhà giao dịch ngắn hạn thường diễn giải điều kiện thị trường theo các cách khác nhau, vì vậy quyết định của bạn nên phản ánh cách tiếp cận cá nhân. Theo phân tích kỹ thuật 4 giờ mới nhất của GMX, tín hiệu giao dịch hiện tại là Hold. Theo phân tích kỹ thuật 1 ngày mới nhất của GMX, tín hiệu hiện tại là Bán.

Dự đoán Beacon

Dự báo giá xác suất cho (24 giờ tới)Tuyên bố miễn trừ trách nhiệm về dự đoán Beacon

Kết quả dữ liệu hiển thị trên trang này được phân tích dựa trên dữ liệu giao dịch thực tế (OHLCV) của cặp giao dịch đã chọn cùng với các chỉ báo kỹ thuật tương ứng.

Dự đoán này là một sản phẩm kỹ thuật thử nghiệm và chỉ được cung cấp để tham khảo. Đây không phải là lời khuyên đầu tư. Những sự kiện bất ngờ trong thế giới thực có thể tác động đáng kể đến hành vi thị trường. Các nhà giao dịch nên đưa ra quyết định một cách thận trọng.

Dự đoán này là một sản phẩm kỹ thuật thử nghiệm và chỉ được cung cấp để tham khảo. Đây không phải là lời khuyên đầu tư. Những sự kiện bất ngờ trong thế giới thực có thể tác động đáng kể đến hành vi thị trường. Các nhà giao dịch nên đưa ra quyết định một cách thận trọng.

Giới thiệu GMX

GMX (GMX) is a cryptocurrency launched in 2021and operates on the Solana platform. GMX has a current supply of 10,430,647.98505698. The last known price of GMX is 5.39623619 USD and is down -0.42 over the last 24 hours. It is currently trading on 477 active market(s) with $2,490,526.31 traded over the last 24 hours. More information can be found at https://gmx.io/.

Đọc thêm

Khám phá thêm

BM Discovery

Mới niêm yết

TIVA Intiva Health

-- 0.00%

LOWON Lowe's

-- 0.00%

ENTGON Entegris

-- 0.00%

CIENON Ciena

-- 0.00%

APOON Apollo Global Management

-- 0.00%

HDON Home Depot

-- 0.00%

TERON Teradyne (Ondo Tokenized)

-- 0.00%

ALABON Astera Labs

-- 0.00%

CNT Centel

-- 0.00%

CRDOON Credo Technology Group Holding Ltd

-- 0.00%

Mua GMX

Giao dịch GMX