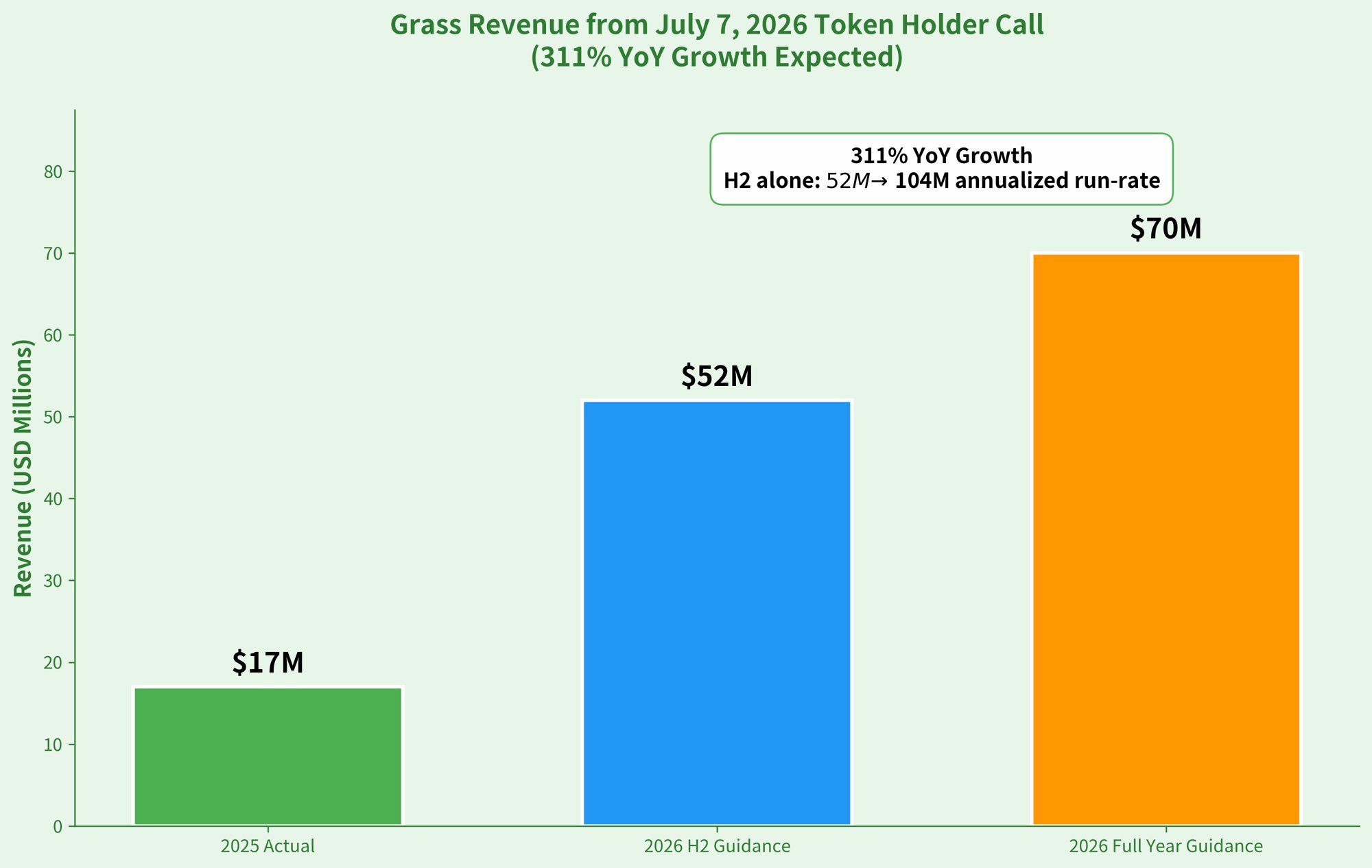

The revenue numbers from the @grass call looked weak yes but going deeper.

They’re deliberately choosing real AI customer revenue (~$17M in 2025 scaling to $65-75M in 2026) to fund rewards instead of diluting $GRASS

This is early-stage infra behavior as they're building enterprise relationships. They've made the decision to protect token scarcity for when LCR inference actually drives usage-based demand.

Current PA is trash I agree and I believe this is going to be longterm game here (something that we aren't used to in crypto)