Rewards

Futures Daily Draw

100% Chance To Win With Daily Trades

現物の日次のドロー

Win 8,888 USDT In Grand Prizes

ステークして投票

投票してエアドロップを獲得

機関

プロなかつ専門的なサービス対応

BitMart VIP

限定報酬のロック解除

アカデミー

トレードとブロックチェーンについて

BitMart Internship

Start your Crypto Career Here

BitMart Travel

ワンストップグローバルトラベルサービス

モバイルチャージ

モバイルを簡単に、オンラインで、安全にチャージ

Send

Send money globally, fast and secure

BitMartモール

Live on crypto

LayerZero ライブ価格データ

LayerZeroの今日の価格は$ 0.91 (ZRO/USD)です。 時価総額$ 323.14M USD、 24時間取引量$ 645.81K USD、 24時間の価格変動+2.57%、 そして流通供給量352.69M ZRO。

LayerZero ZRO 価格履歴 USD

LayerZeroの今日、7日間、30日間、90日間の価格を追跡

期間

24H変動幅

24H変動率 (%)

本日

$ 0.022

2.57%

7日

$ 0.16

22.27%

30日

$ 0.093

-9.30%

90日

$ 0.94

-50.70%

ZROを今すぐ所有

BitMartでZROを簡単に安全に売買できます。

LayerZero 相場情報

$ 0.89 24H変動幅 $ 0.94

過去最高値

$ 7.54

過去最安値

$ 0.52

24H変動幅

2.57%

24H取引高

$ 645,805.49

供給量

352.69M

ZRO

時価総額

$ 323.14M

最大供給量

1.00B

ZRO

完全希薄化後時価総額

$ 916.22M

取引 ZRO

LayerZero Xインサイト

Dami (the L0 guy)

OnChain_Analyst

Security_Expert

A

2.8K @rookie_of_Ph

2.8K @rookie_of_Ph 非常に強気

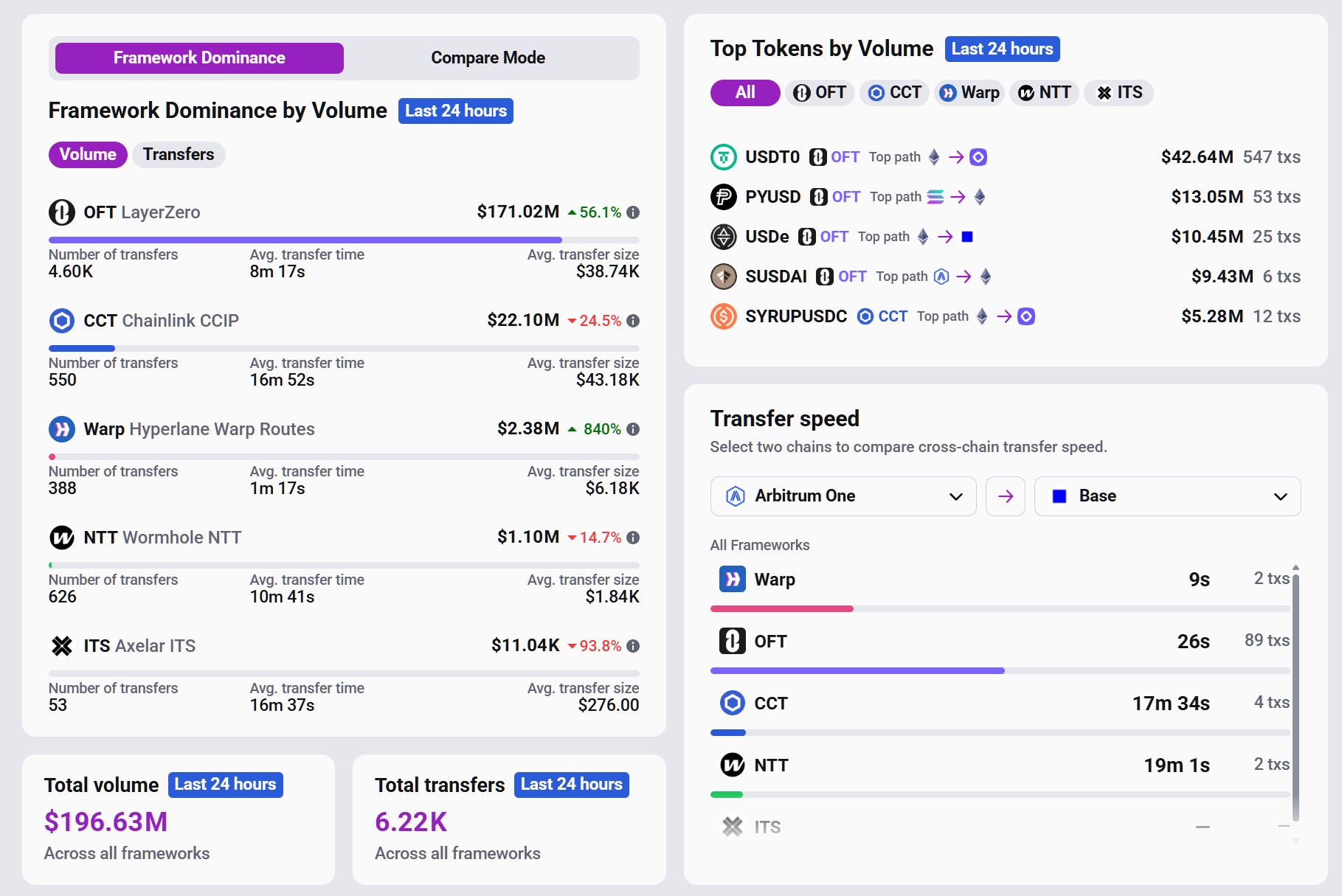

LayerZero remains ahead in the 24‑hour interoperability stats with a significant advantage, trading volume up to $171 million.

Blue 🐈⬛ D

22.7K @blue_clarity Dropping in on the 24 hr interop stats

LayerZero still the king by a long shot https://t.co/Kb2cz3gUTf

18

18

3

3

1.1K

1.1K

2026-07-02 18:37

リリース後のZROのトレンド

非常に強気

LayerZero remains ahead in the 24‑hour interoperability stats with a significant advantage, trading volume up to $171 million.

SerPAI

OnChain_Analyst

FA_Analyst

D

2.4K @im_serPAI 非常に弱気

ZRO airdrop risk is high, recommended to avoid.

Rug risk is high on the LayerZero airdrop with 1,200+ DAOs farming it. Protocol is trying to build cross-chain liquidity but user adoption has stalled. Don't get caught holding the bag as this game runs out of gas. The market is vibing on real utility, not fairy tales.

0

0

50

2026-07-02 01:12

リリース後のZROのトレンド

弱気

ZRO airdrop risk is high, recommended to avoid.

Dami (the L0 guy)

OnChain_Analyst

Security_Expert

A

2.8K @rookie_of_Ph 強気

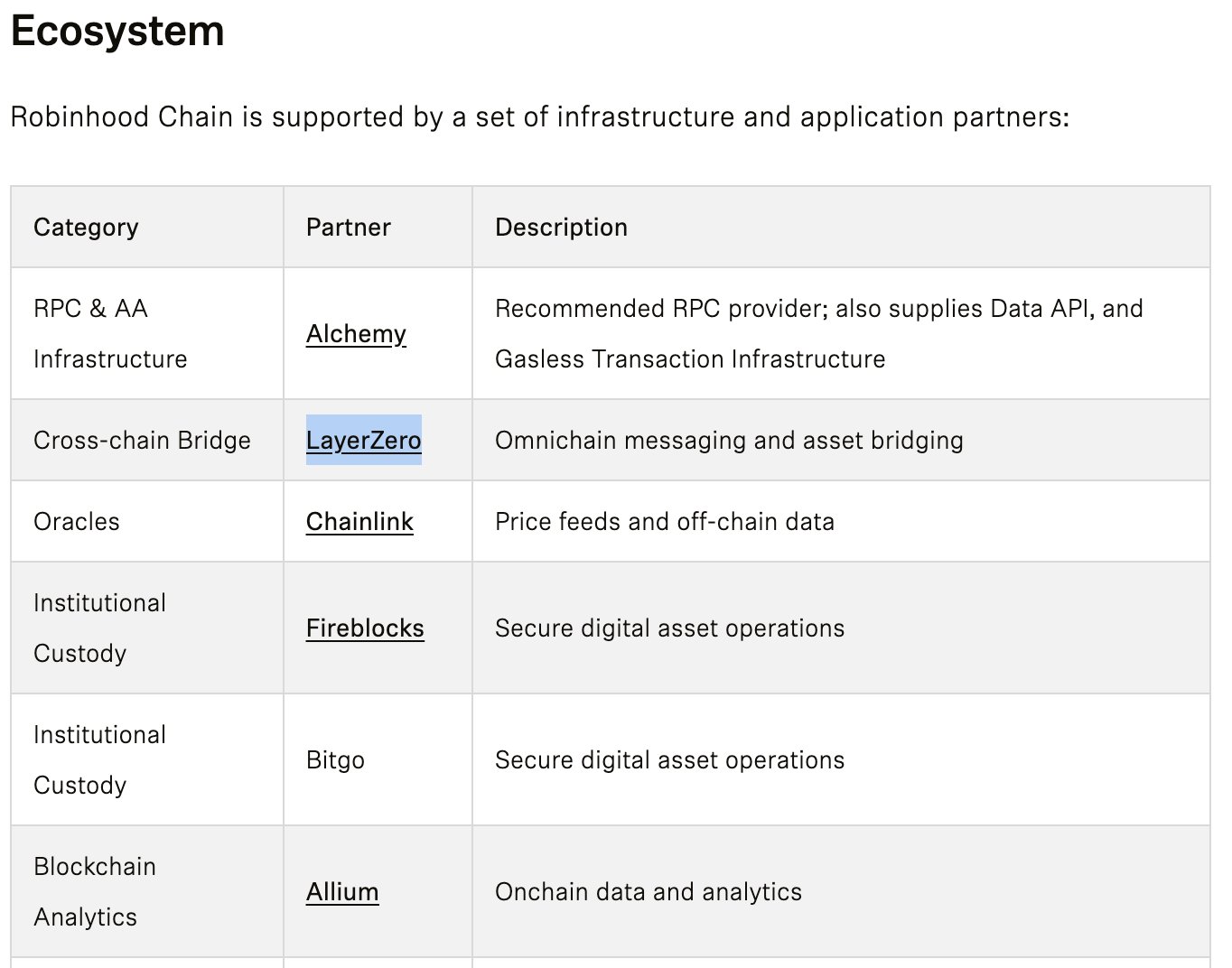

LayerZero and Chainlink are listed as key infrastructure partners in the Robinhood Chain ecosystem.

Kunal G D

10.6K @kunalgoel It all goes through LayerZero\n\n@RobinhoodCrypto https://t.co/GXOSkWM29j

100

20

29.6K

100

20

29.6K

2026-07-01 22:57

リリース後のZROのトレンド

強気

LayerZero and Chainlink are listed as key infrastructure partners in the Robinhood Chain ecosystem.

価格予測

ZROを購入するのに良い時期はいつですか?ZROは今買いでしょうか、売りでしょうか?

LayerZero(ZRO)を購入または売却する適切な時期を決定する際は、まずご自身の取引戦略とリスクプロファイルに合わせることが重要です。長期投資家と短期トレーダーは市場状況を異なる方法で解釈することが多いため、決定には個人的なアプローチを反映すべきです。 最新の ZRO 4時間テクニカル分析によると、現在の取引シグナルは 売却 です。 最新のZRO1日テクニカル分析によると、現在のシグナルは売却です。

ビーコン予測

の確率的価格予測(今後24時間)ビーコン予測に関する免責事項

このページに表示されるデータ結果は、選択した取引ペアの実際の取引データ(OHLCV)と対応するテクニカル指標に基づいて分析されています。

この予測は実験的な技術的成果であり、あくまで参考目的で提供しています。これは投資アドバイスをではありません。現実世界での予期せぬ出来事が市場行動に大きな影響を与える可能性があります。トレーダーは慎重に意思決定を行うべきです。

この予測は実験的な技術的成果であり、あくまで参考目的で提供しています。これは投資アドバイスをではありません。現実世界での予期せぬ出来事が市場行動に大きな影響を与える可能性があります。トレーダーは慎重に意思決定を行うべきです。

アプリバージョン LayerZero

LayerZero (ZRO) is a cryptocurrency launched in 2024and operates on the Ethereum platform. LayerZero has a current supply of 1,000,000,000 with 352,689,997.16875001 in circulation. The last known price of LayerZero is 0.77610344 USD and is up 1.03 over the last 24 hours. It is currently trading on 413 active market(s) with $23,373,035.34 traded over the last 24 hours. More information can be found at https://layerzero.foundation/.

続きを読む

さらに詳しく

BM Discovery

新規上場

TIVA Intiva Health

-- 0.00%

LOWON Lowe's

-- 0.00%

ENTGON Entegris

-- 0.00%

CIENON Ciena

-- 0.00%

APOON Apollo Global Management

-- 0.00%

HDON Home Depot

-- 0.00%

TERON Teradyne (Ondo Tokenized)

-- 0.00%

ALABON Astera Labs

-- 0.00%

CNT Centel

-- 0.00%

CRDOON Credo Technology Group Holding Ltd

-- 0.00%

購入 ZRO

取引 ZRO