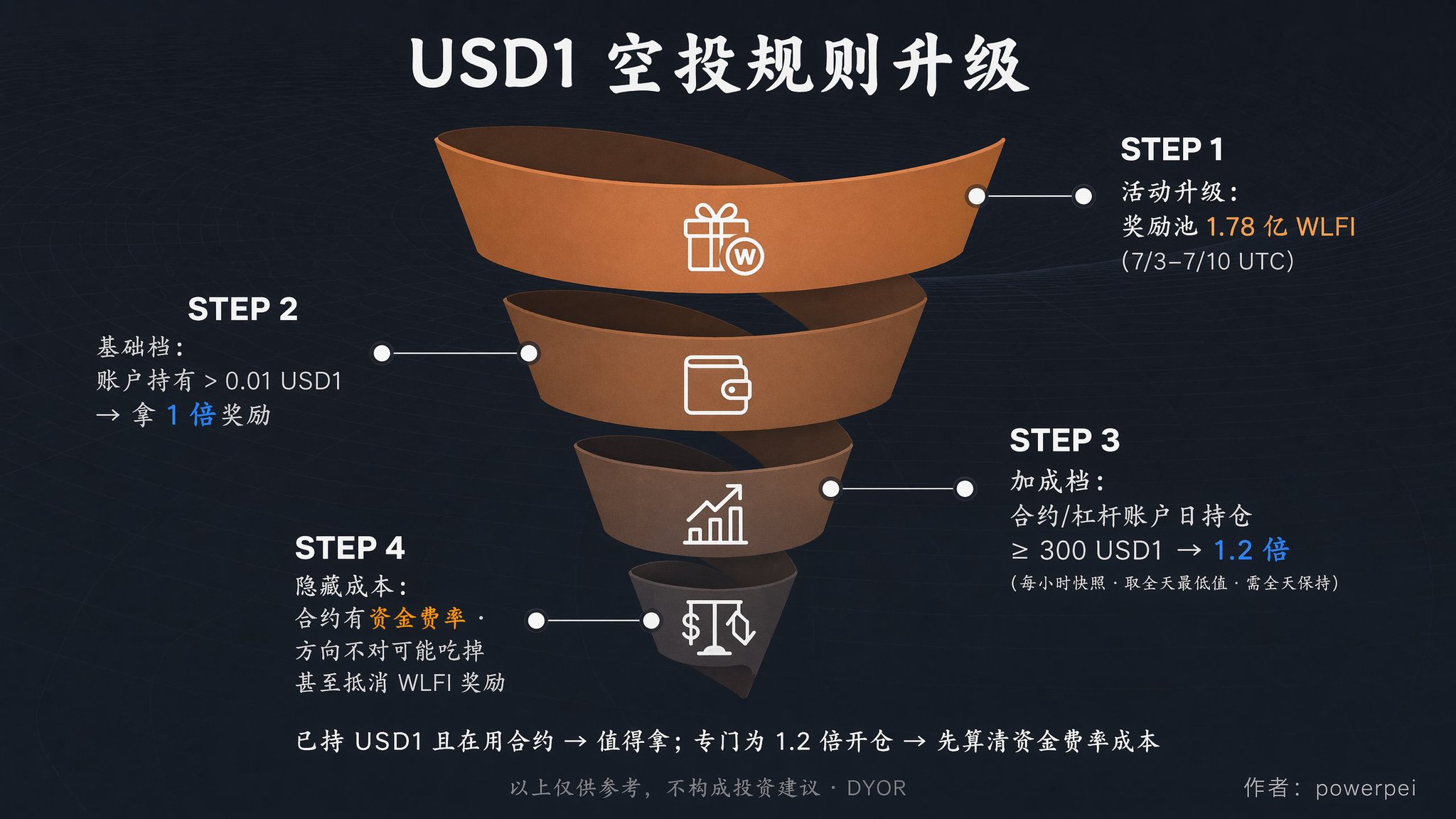

Binance USD1's airdrop rules were updated yesterday

There's a detail worth mentioning

Effective from 00:00 UTC on July 3, the campaign ends on July 10, with a total reward pool of 178 million WLFI

─────────────────────

The rule change is simple: previously holding USD1 earned rewards, now a new condition is added

Place USD1 in a futures or margin account, and maintain a daily position of at least 300 USD1 to receive a 1.2× multiplier

Binance snapshots once per hour and uses the lowest value of the day for calculation, so you must keep the position all day, cannot turn it on and off

If you don't reach 300 but have more than 0.01 USD1 in the account, you still get the base reward at 1×

─────────────────────

Things I think are worth noting

300 USD1 is roughly $300, the threshold is not high

Binance uses this design to bring USD1 into the futures market, increasing liquidity; the platform benefits, users get more rewards, which is a win‑win in principle.

But one thing many people didn't mention

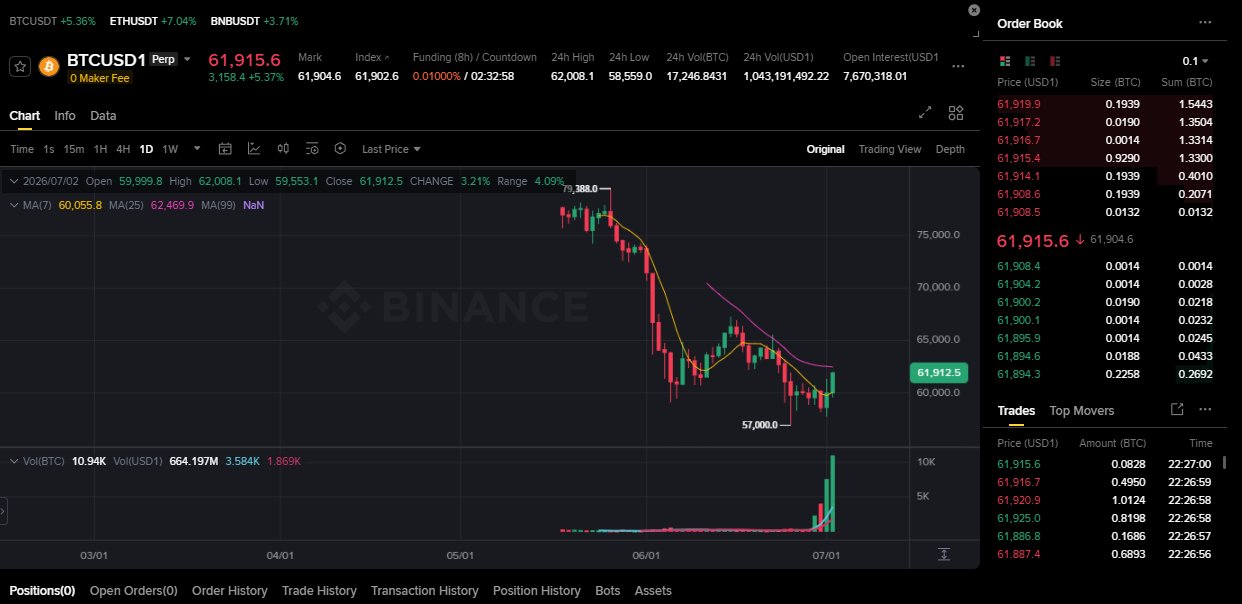

Futures positions have funding rates. The funding rate is a fee paid between long and short sides every few hours, its direction and amount change daily and are not fixed

If the funding rate direction is unfavorable, this cost can eat up part or even all of the extra WLFI rewards.

Some community members discuss hedging to bypass this issue, but the operation is complex. Others complain that Binance support is slow; it took several days to confirm the rule details.

My view: for those already holding USD1 and using a futures account, this multiplier is worthwhile.

If you open a futures position solely for the 1.2× boost, first calculate the funding rate cost before deciding, don't focus only on the reward side.

This is for reference only and does not constitute investment advice. DYOR