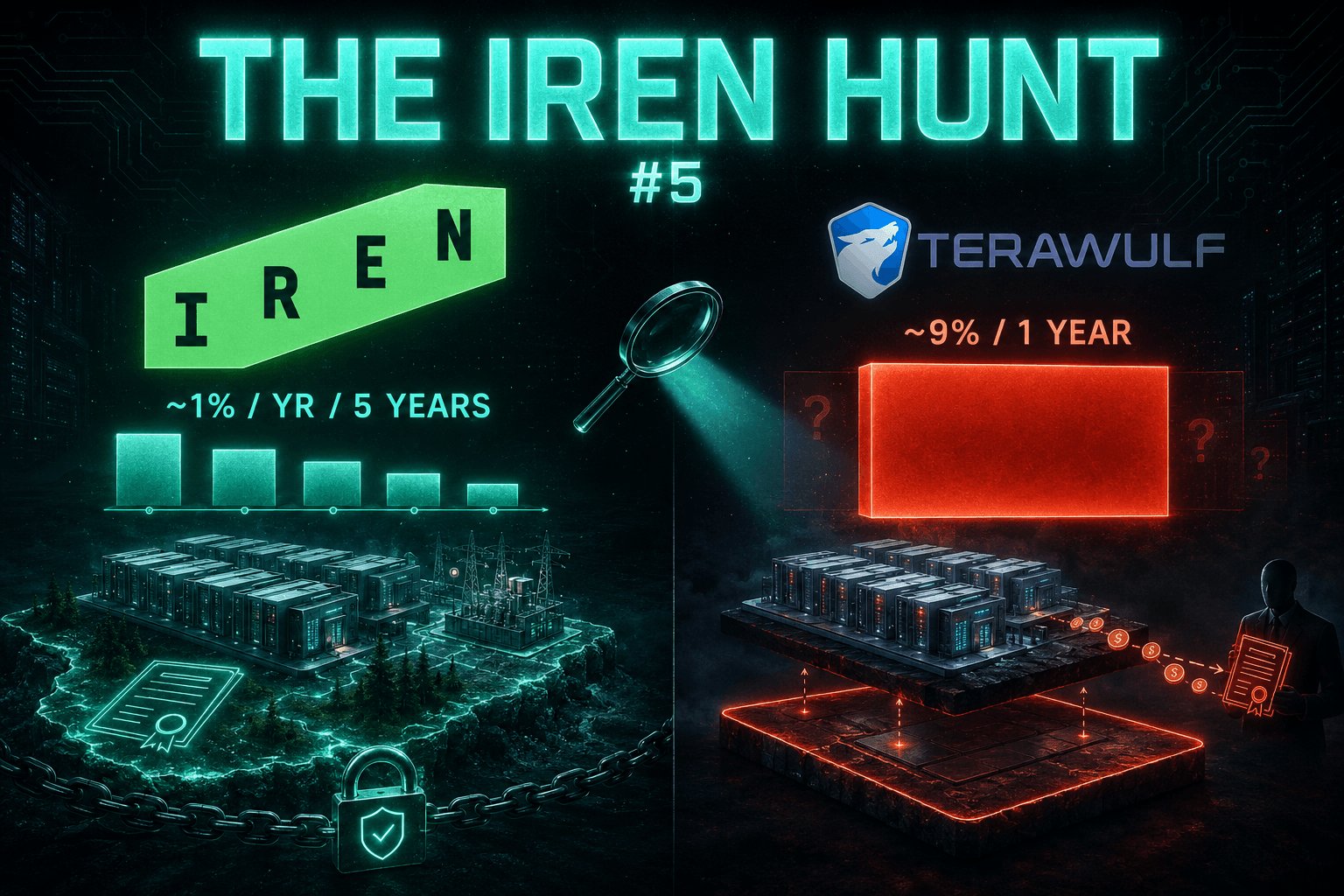

The $IREN Hunt #5: $WULF.

The series continues.

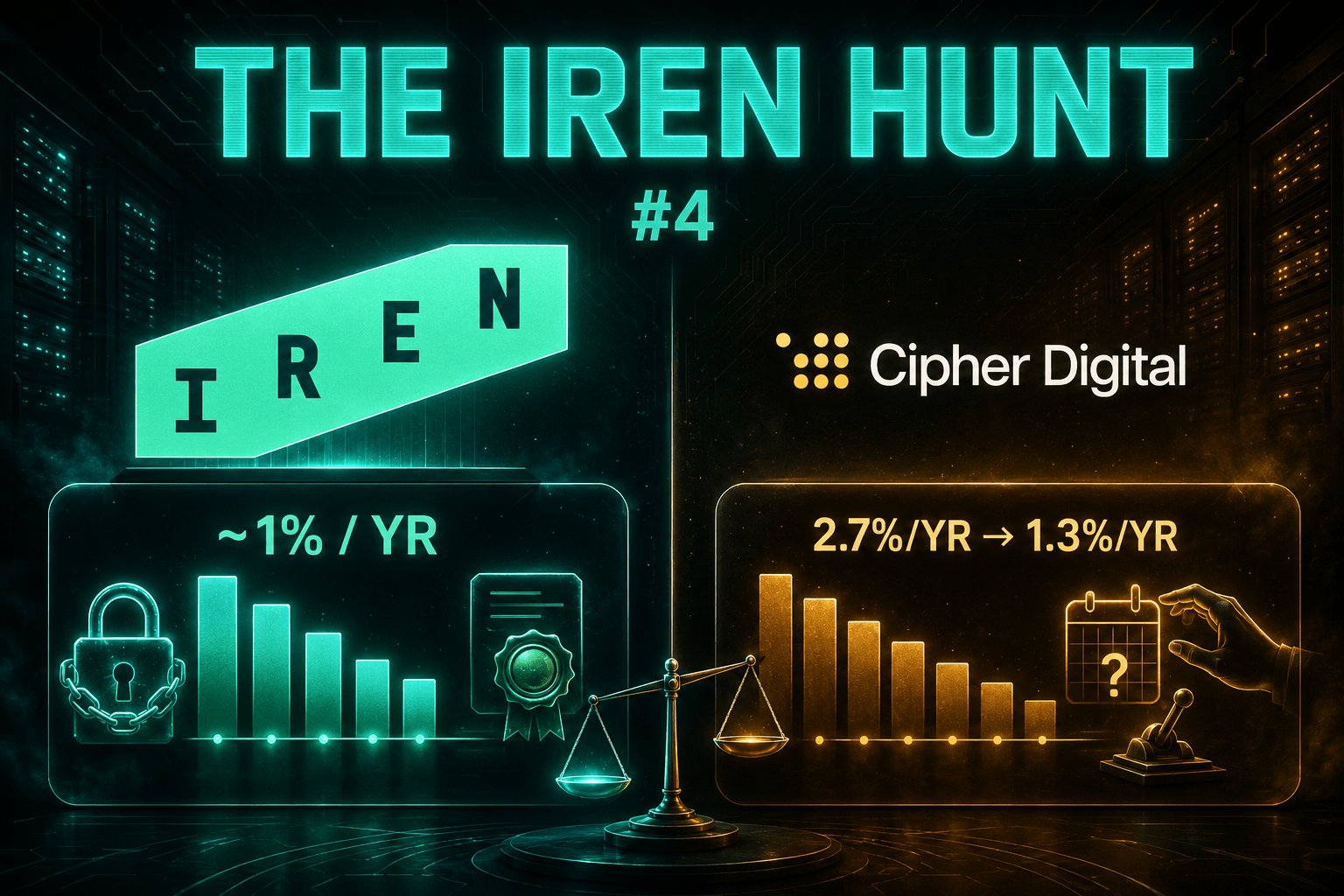

Last hunt: $CIFR, the control group, proof this space CAN do comp reasonably.

Today we go back to the dark side, because WULF's story isn't in the comp table at all.

TeraWulf.

And the most creative founder-equity structure I've found: the money doesn't flow through compensation. It flows through the land.

Flavor one, the visible one: comp.

Per the proxy...

➟ CEO Paul Prager took 2.5M RSUs in the 2025 round.

➟ CSO Kerri Langlais 1.5M, the COO a comparable award.

➟ Prager's 2025 total comp: ~$39.4M.

Roughly 1.5% of the company for the founding trio.

Aggressive, but survivable. If that were the whole story, WULF might pass like CIFR did.

It's not the whole story.

Flavor two, the one most retail never reads: related-party land deals.

October 2024: TeraWulf paid 20 million shares plus $12M cash to Riesling Power LLC, an entity controlled by its own CEO, to terminate and renegotiate the Lake Mariner ground lease.

Straight from the 8-K.

August 2025: TeraWulf paid another 15 million shares, roughly $95M, plus $3M cash to the same CEO-controlled entity, for an 80-year lease at Lake Hawkeye.

That's 35 million shares.

Roughly 9% of the company, flowing to entities controlled by the CEO in under a year.

On top of comp.

The company pays rent, for decades, on land its own CEO's entity controls.

And the lockup on those 20M Lake Mariner shares?

5 million sellable after 12 months.

ALL of them unrestricted after April 2026.

Eighteen months, total.

That date has already passed.

Now put IREN next to that, piece by piece.

The land.

IREN's shareholders OWN it.

Freehold sites, company-owned substations.

Prince George, Childress, Sweetwater: the dirt, the buildings, the grid connections sit on IREN's balance sheet.

Nobody's LLC collects rent on them for 80 years.

When you buy IREN, the landlord is YOU.

Forever.

The equity.

A fixed 18.2M shares combined, ~5.1% once, covering five years of comp, shrinking as a slice every year the share count grows.

Zero additional equity until fiscal 2031, in writing.

Not one share sellable before 2029, and after that the unlocks are staggered at roughly 25% a year through 2032.

So run the honest comparison.

One structure: ~9% of the company to CEO-controlled entities in ten months, plus annual comp on top, fully sellable within eighteen months, with the company as a rent-paying tenant on its own flagship sites.

The other: ~1% a year and shrinking, all comp, zero related-party landlords, first sellable share three years out, ceiling sealed until 2031.

You can dislike the size of IREN's grant.

I've said so myself.

But if you're angry at IREN and quiet about structures like this one, you're not doing analysis.

You're doing vibes.

Do you have any suggestions?

Drop it in the comments.

The Hunt continues.

Next ticker soon.

This is not financial advice. Do your own research.

I am long $IREN.

IREN (IREN)

IREN (IREN) Jake Wujastyk 技术分析师 教育者 C397.30K @Jake__Wujastyk

Jake Wujastyk 技术分析师 教育者 C397.30K @Jake__Wujastyk 213 39 53.36K 阅读原文 >发布后IREN走势中性

213 39 53.36K 阅读原文 >发布后IREN走势中性