IREN (IREN)

IREN (IREN)

- 61社交熱度指數(SSI)-13.84% (24h)

- #60市場預警排名(MPR)+27

- 924小時社交提及量-18.18% (24h)

- 77%24小時KOL看好比例6位活躍KOL

- 概要IREN announced governance audit received positive reviews, technical falling wedge support manifested, price slipped slightly, social heat declined, institutional attention rose.

- 看漲訊號

- Audit says governance is rigorous

- Plan to upgrade independent AI board

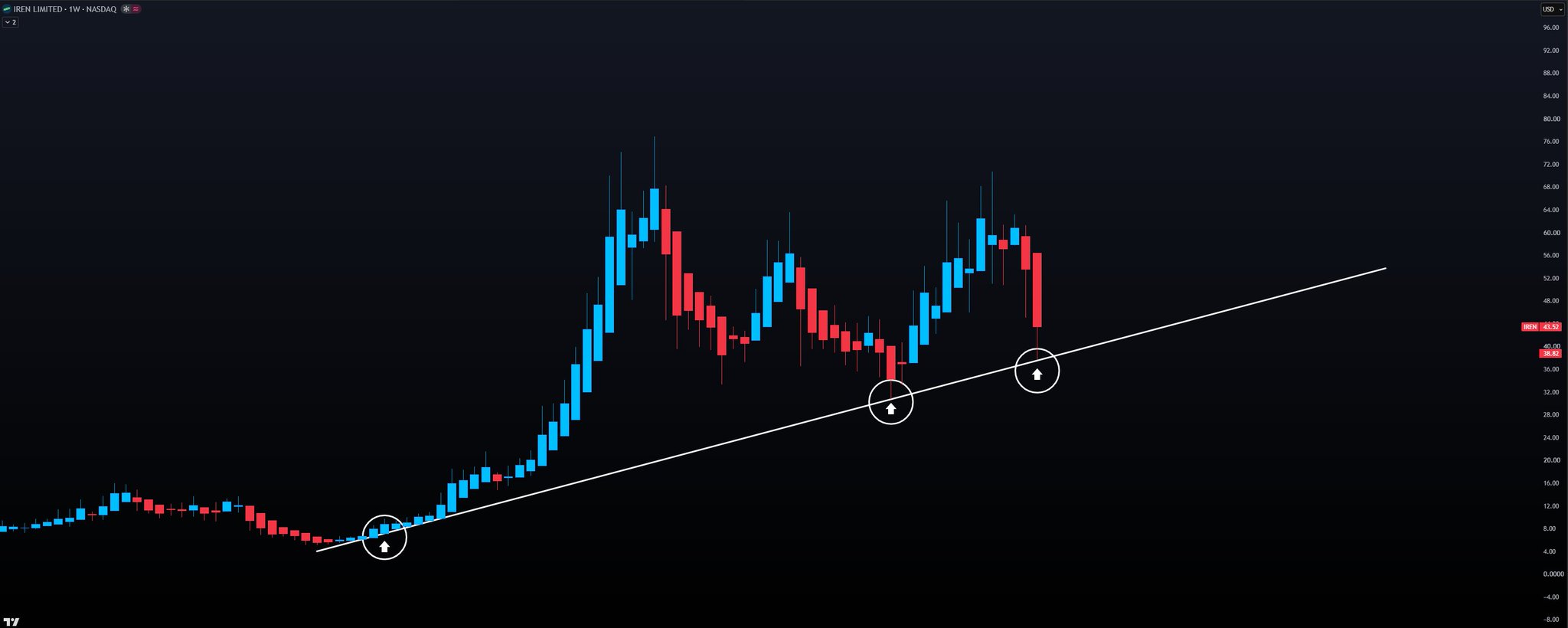

- Falling wedge breaks support at 38.82

- RSI low at 30.58, oversold

- Institutions continue to increase holdings

- 看跌訊號

- Price down 0.46% in 24h

- Social heat down 13.8%

- Jake questions upward momentum

- Founder high compensation concerns

- Short sellers have finished playing

社交熱度指數(SSI)

- 總體資料61SSI

- 社交熱度趨勢(7D)價格(7D)情緒分佈極度看漲 (33%)看漲 (44%)中性 (23%)社交熱度洞察IREN social heat is moderate (61.33/100, -13.84%), activity sharply dropped -21.25% and KOL attention -58.06%, positive sentiment ↑48.79%, due to positive audit reviews and slight price dip causing attention shift.

市場預警排名(MPR)

- 預警解讀IREN warning rank rose to #60 (+27), sentiment polarization surged to 35.08/100 (+1437%) as the main anomaly, reflecting sentiment divergence caused by positive audit reviews and institutional accumulation.

相關推文

Black Panther Capital FA_Analyst Researcher S43.31K @BlackPantherCap

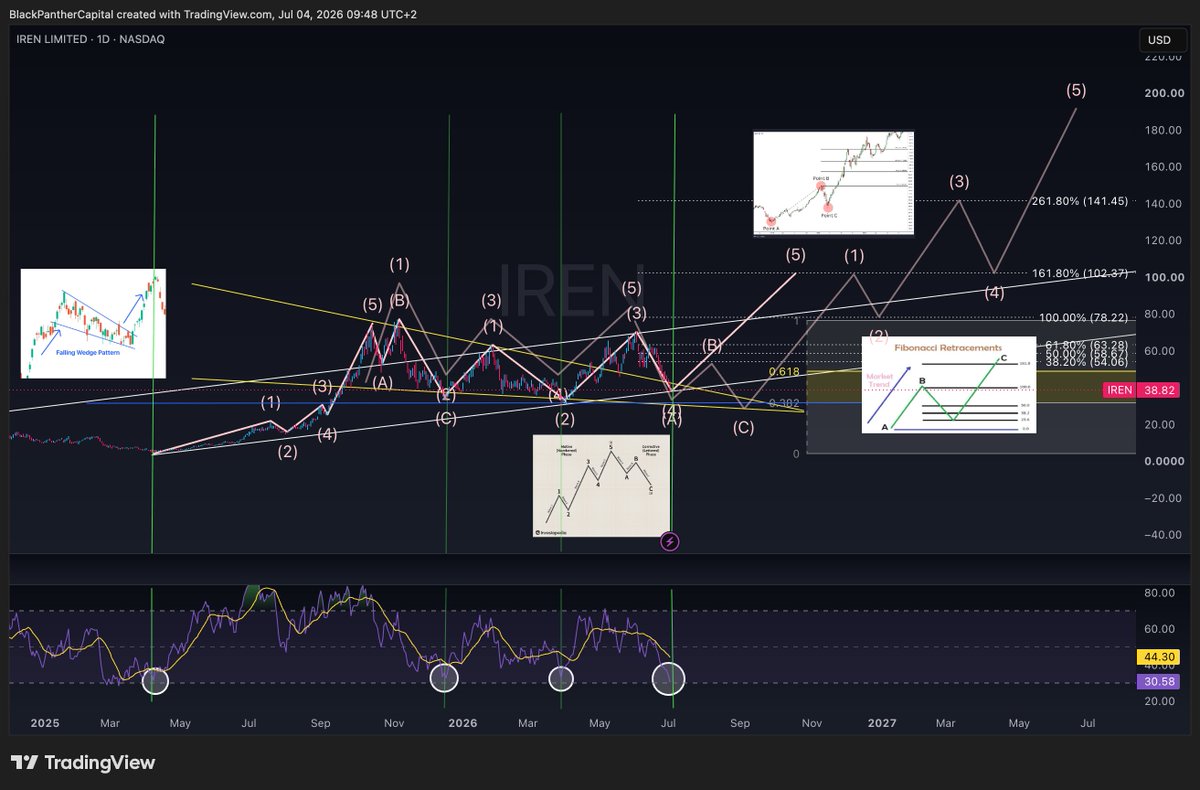

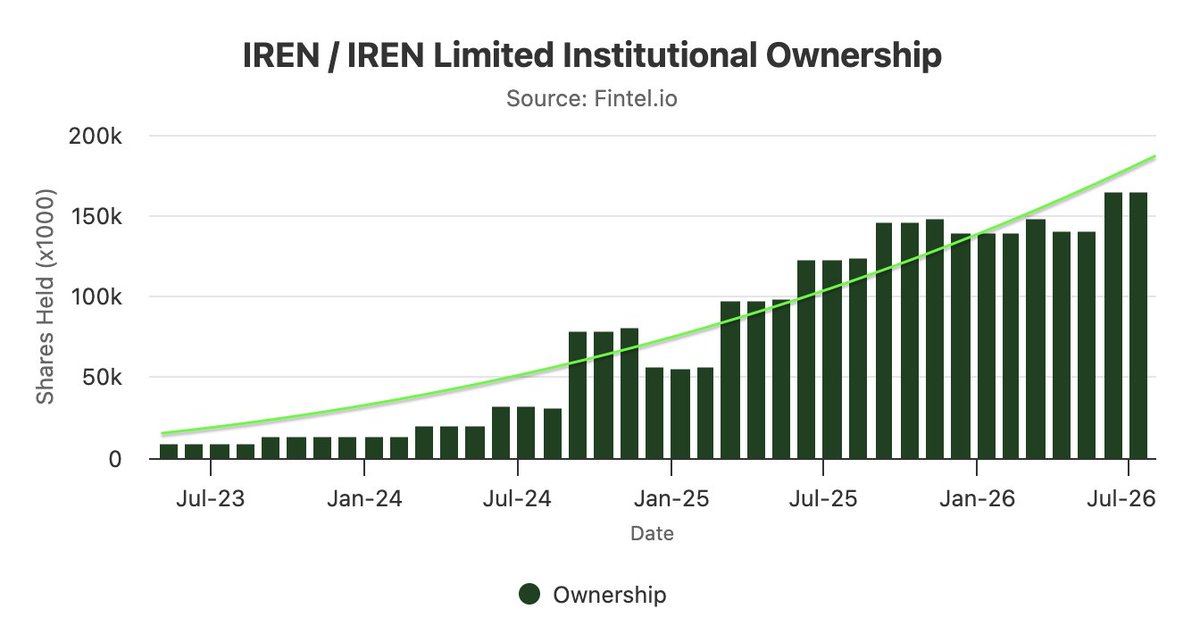

Black Panther Capital FA_Analyst Researcher S43.31K @BlackPantherCapTaking a deep dive into the $IREN daily chart on and the technical setup is looking incredibly precise right now. The bears have had their fun, but the structural foundations are hinting that a massive shift could be just around the corner. > A clear falling wedge pattern acted as the original breakout catalyst to kickstart the macro bullish sequence. > The deep retracement invalidates a standard Wave 4 impulse, making a major ABC corrective structure the highly probable scenario. > The current price down at 38.82 aligns perfectly with macro trendline support and the key 38.2% Fibonacci retracement level. > The daily Relative Strength Index has plummeted down to 30.58, indicating deeply oversold conditions and potential seller exhaustion at this key junction. > Holding this structural support pivot sets the stage for the next macro cycle, targeting the 161.8% extension level up near 102.37. > Institutional Ownership still growing and accumulating. The chart structure on shows a textbook alignment of wave counts, Fibonacci levels, and oversold momentum signals. Keep a very close eye on how the price handles this current accumulation zone. -BP Please note, as always this is not financial advice.

50 5 6.33K 閱讀原文 >釋出後IREN走勢極度看漲IREN technicals show oversold conditions and increasing institutional holdings, expected to start a new macro uptrend cycle, target price 102.37.

50 5 6.33K 閱讀原文 >釋出後IREN走勢極度看漲IREN technicals show oversold conditions and increasing institutional holdings, expected to start a new macro uptrend cycle, target price 102.37. ChinoAleman D7.39K @chinoalemano

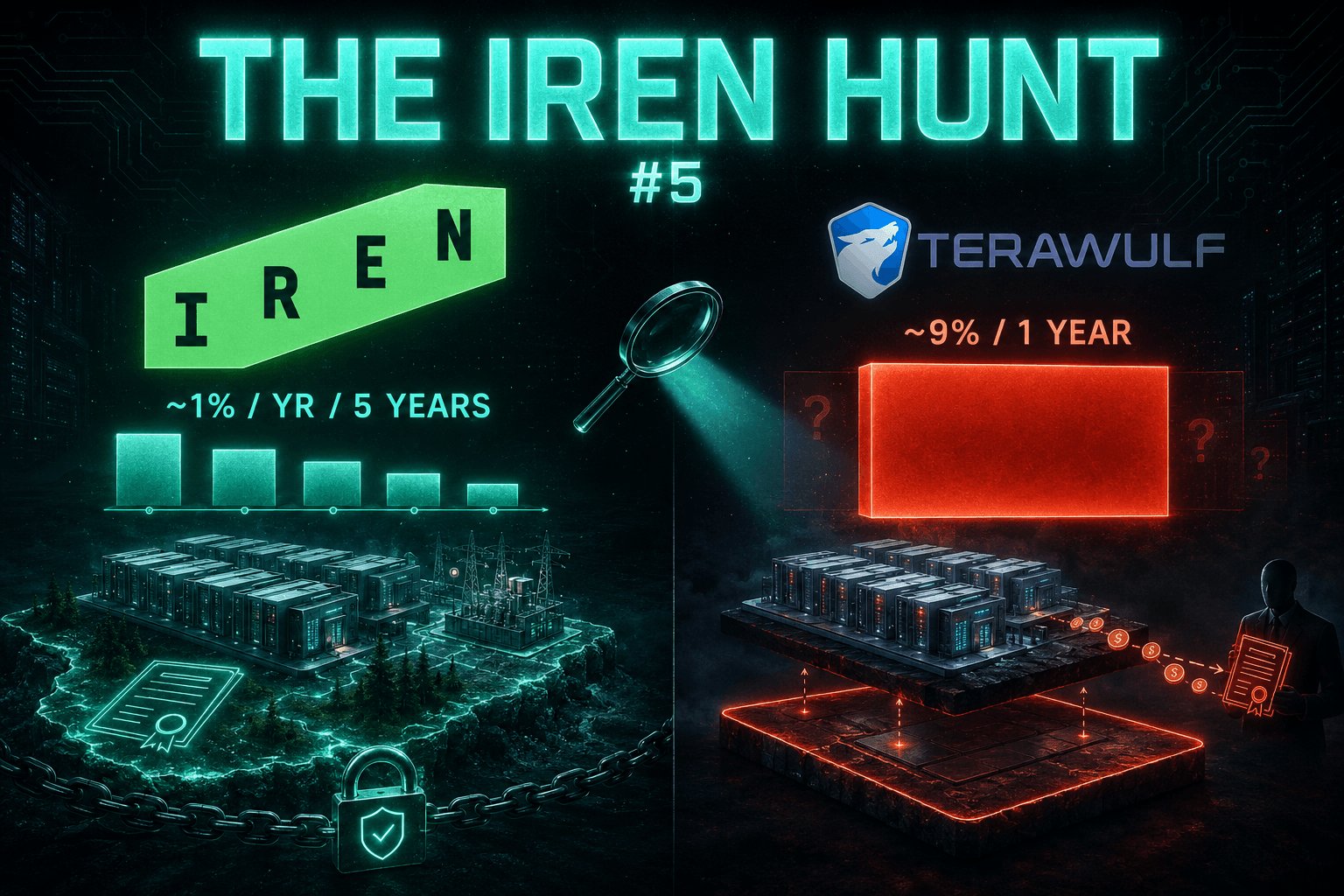

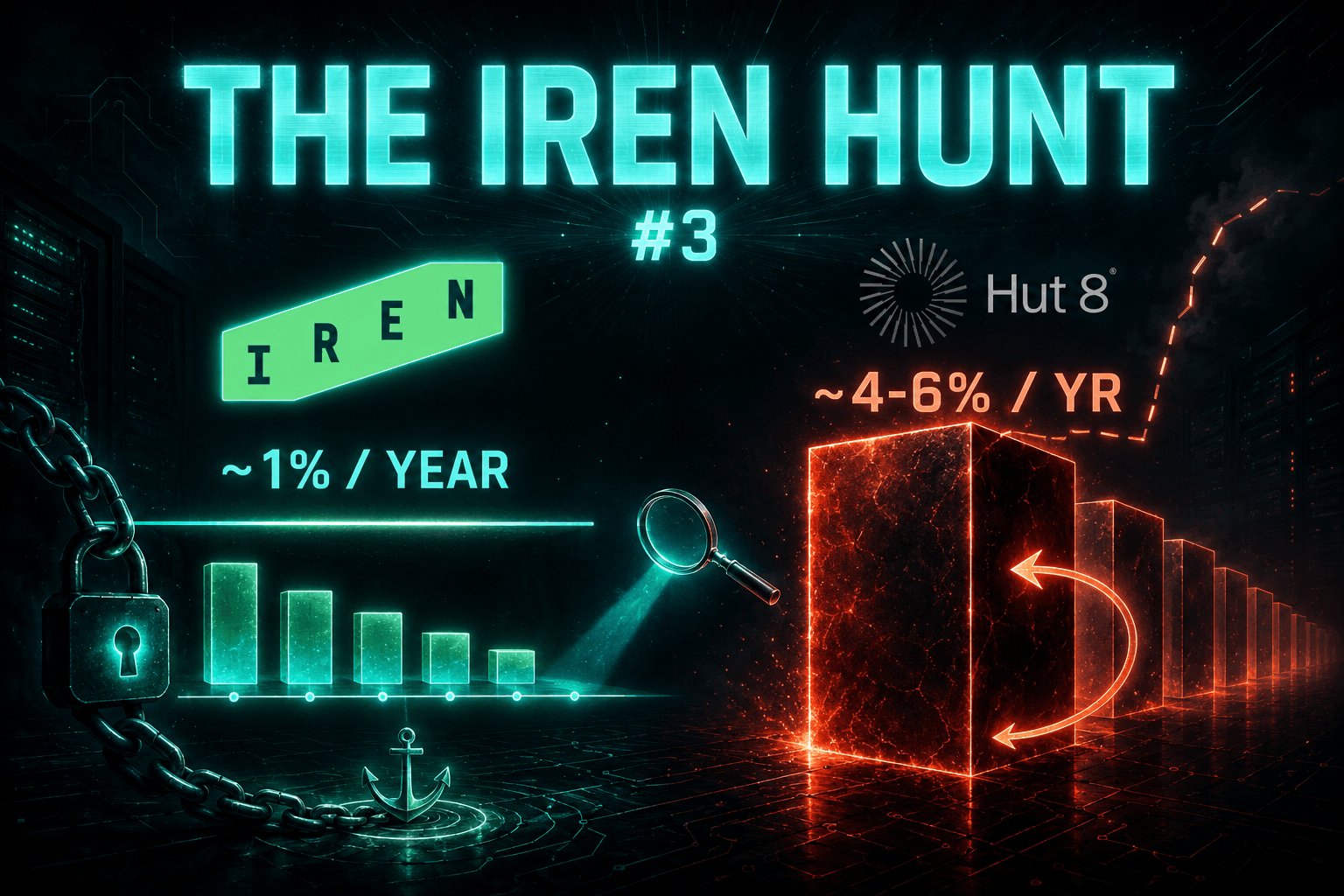

ChinoAleman D7.39K @chinoalemanoThe $IREN Hunt #5: $WULF. The series continues. Last hunt: $CIFR, the control group, proof this space CAN do comp reasonably. Today we go back to the dark side, because WULF's story isn't in the comp table at all. TeraWulf. And the most creative founder-equity structure I've found: the money doesn't flow through compensation. It flows through the land. Flavor one, the visible one: comp. Per the proxy... ➟ CEO Paul Prager took 2.5M RSUs in the 2025 round. ➟ CSO Kerri Langlais 1.5M, the COO a comparable award. ➟ Prager's 2025 total comp: ~$39.4M. Roughly 1.5% of the company for the founding trio. Aggressive, but survivable. If that were the whole story, WULF might pass like CIFR did. It's not the whole story. Flavor two, the one most retail never reads: related-party land deals. October 2024: TeraWulf paid 20 million shares plus $12M cash to Riesling Power LLC, an entity controlled by its own CEO, to terminate and renegotiate the Lake Mariner ground lease. Straight from the 8-K. August 2025: TeraWulf paid another 15 million shares, roughly $95M, plus $3M cash to the same CEO-controlled entity, for an 80-year lease at Lake Hawkeye. That's 35 million shares. Roughly 9% of the company, flowing to entities controlled by the CEO in under a year. On top of comp. The company pays rent, for decades, on land its own CEO's entity controls. And the lockup on those 20M Lake Mariner shares? 5 million sellable after 12 months. ALL of them unrestricted after April 2026. Eighteen months, total. That date has already passed. Now put IREN next to that, piece by piece. The land. IREN's shareholders OWN it. Freehold sites, company-owned substations. Prince George, Childress, Sweetwater: the dirt, the buildings, the grid connections sit on IREN's balance sheet. Nobody's LLC collects rent on them for 80 years. When you buy IREN, the landlord is YOU. Forever. The equity. A fixed 18.2M shares combined, ~5.1% once, covering five years of comp, shrinking as a slice every year the share count grows. Zero additional equity until fiscal 2031, in writing. Not one share sellable before 2029, and after that the unlocks are staggered at roughly 25% a year through 2032. So run the honest comparison. One structure: ~9% of the company to CEO-controlled entities in ten months, plus annual comp on top, fully sellable within eighteen months, with the company as a rent-paying tenant on its own flagship sites. The other: ~1% a year and shrinking, all comp, zero related-party landlords, first sellable share three years out, ceiling sealed until 2031. You can dislike the size of IREN's grant. I've said so myself. But if you're angry at IREN and quiet about structures like this one, you're not doing analysis. You're doing vibes. Do you have any suggestions? Drop it in the comments. The Hunt continues. Next ticker soon. This is not financial advice. Do your own research. I am long $IREN.

ChinoAleman D7.39K @chinoalemano

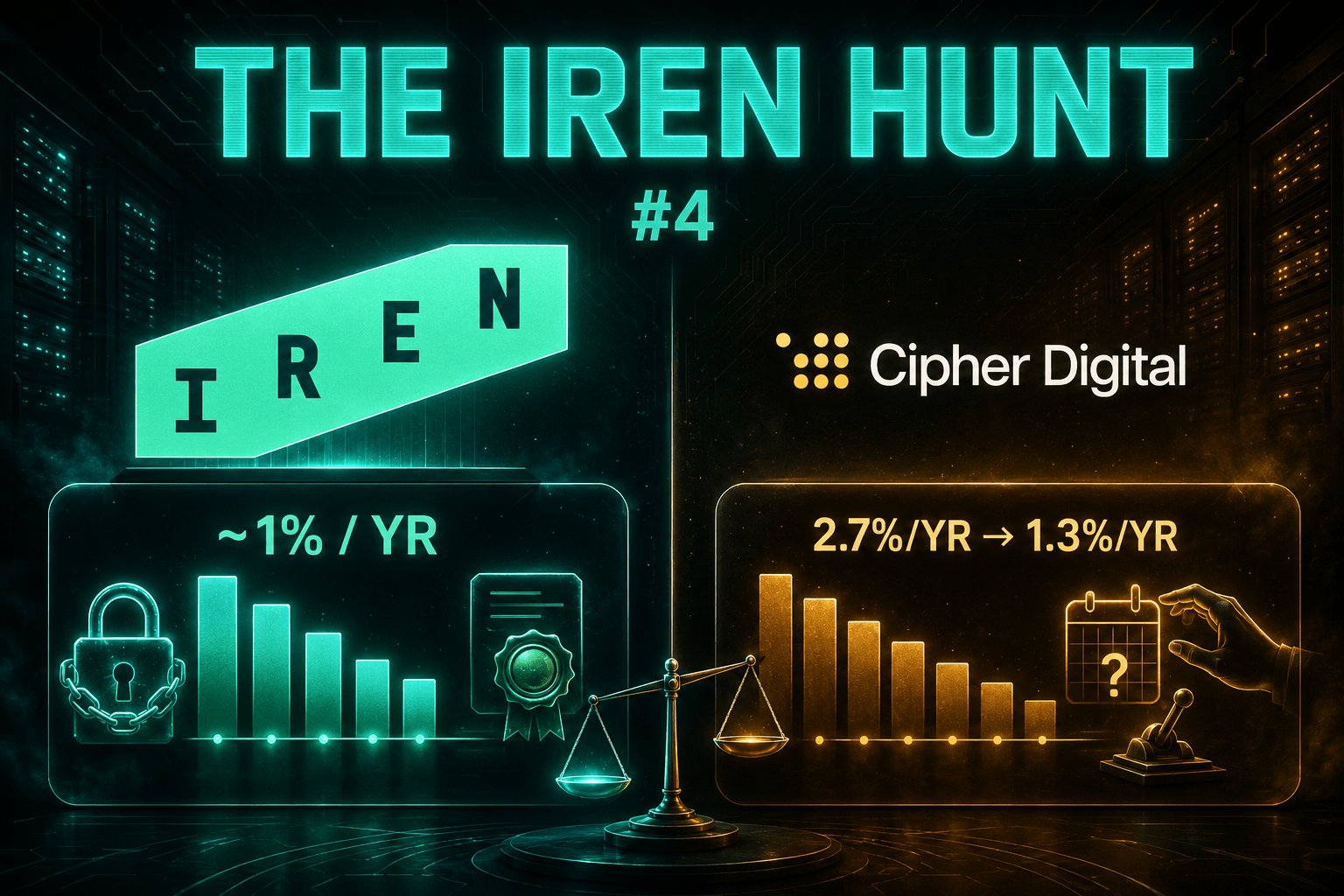

ChinoAleman D7.39K @chinoalemanoThe $IREN Hunt #4: $CIFR. This chapter is different. And that difference is the point. The Hunt isn't a hit-piece series. It's an audit. And an audit that only ever finds villains isn't an audit, it's a script. So today: the peer that mostly passes. Cipher Mining. Bitcoin miner turned AI datacenter play, AWS and Fluidstack/Google leases, ~3.2 GW pipeline. The numbers, from the filings. CEO Tyler Page received: ~1.6% of the company in 2024 (a front-loaded year), ~0.75% in 2025. ~0.75% projected (more or less) for 2026. The full exec team: roughly 2.7%, then ~1.3%, stabilizing around ~1.3% a year, with Page consistently taking just under 60% of the exec pool. Credit where due. The Hunt is honest or it's nothing: ➟ The percentages DECLINE every year. ➟ Independent chair. ➟ Clawback policy. ➟ Anti-hedging. ➟ PSUs tied to market-cap hurdles. ➟ Moderate sizes, orthodox split. Of everything I've hunted so far, this is by far the most disciplined structure. NUAI and SLNH should take notes. Now, h

39 2 2.45K 閱讀原文 >釋出後IREN走勢極度看漲The equity and land ownership structure of IREN is superior to the problematic transaction of WULF; the author is bullish on IREN.

39 2 2.45K 閱讀原文 >釋出後IREN走勢極度看漲The equity and land ownership structure of IREN is superior to the problematic transaction of WULF; the author is bullish on IREN. Luke ₿ TA_Analyst Trader B3.04K @LukeDavisgrey

Luke ₿ TA_Analyst Trader B3.04K @LukeDavisgrey“Support” https://t.co/ijB1eYGCB7

Mind Investor D37.48K @mind1nvestor

Mind Investor D37.48K @mind1nvestor$IREN Two perfect reactions from this trendline. Yesterday it was tested for the third time. The crowd has a remarkable talent for turning bearish at support. https://t.co/ua4fidiWMb

1 0 182 閱讀原文 >釋出後IREN走勢看漲IREN price got a perfect reaction at the key upward trendline support level, the author holds a bullish rebound view.

1 0 182 閱讀原文 >釋出後IREN走勢看漲IREN price got a perfect reaction at the key upward trendline support level, the author holds a bullish rebound view. AISavvy Trader FA_Analyst B8.35K @AISavvyCapital

AISavvy Trader FA_Analyst B8.35K @AISavvyCapitalI’ve traded $iren for almost a year perfectly , maybe a little luck too - I’m buying again down here https://t.co/0S8bX1FnRd

3 0 351 閱讀原文 >釋出後IREN走勢看漲The author, based on a perfect trading record in the past, buys IREN again during its current decline, bullish on its future performance.

3 0 351 閱讀原文 >釋出後IREN走勢看漲The author, based on a perfect trading record in the past, buys IREN again during its current decline, bullish on its future performance. Jake Wujastyk TA_Analyst Educator C397.30K @Jake__WujastykJake Wujastyk TA_Analyst Educator C397.30K @Jake__Wujastyk

Jake Wujastyk TA_Analyst Educator C397.30K @Jake__WujastykJake Wujastyk TA_Analyst Educator C397.30K @Jake__Wujastyk$IREN #IREN Hard to see this happening, but it is one option. https://t.co/suQsSEfarx

202 39 50.47K 閱讀原文 >釋出後IREN走勢中性IREN's price is in a downtrend, and the chart shows it could fall to the $28-34 support zone, but the author is skeptical about this.

202 39 50.47K 閱讀原文 >釋出後IREN走勢中性IREN's price is in a downtrend, and the chart shows it could fall to the $28-34 support zone, but the author is skeptical about this. Seth FA_Analyst Trader C95.22K @seth_fin

Seth FA_Analyst Trader C95.22K @seth_fin$IREN retesting the demand zone Resistance line and the weekly cloud should act as support here at $38.82 Bitcoin miner that also serve as a high-performance AI infrastructure provider #IREN https://t.co/PQW56gUjqD

24 7 5.95K 閱讀原文 >釋出後IREN走勢看漲IREN stock price finds $38.82 support in the demand zone, with technical levels expected to play a role.

24 7 5.95K 閱讀原文 >釋出後IREN走勢看漲IREN stock price finds $38.82 support in the demand zone, with technical levels expected to play a role.- Jake Wujastyk TA_Analyst Educator C397.30K @Jake__Wujastyk

$IREN #IREN Hard to see this happening, but it is one option. https://t.co/suQsSEfarx

202 39 50.47K 閱讀原文 >釋出後IREN走勢中性IREN's price is in a downtrend, and the chart shows it could fall to the $28-34 support zone, but the author is skeptical about this. - ChinoAleman D7.39K @chinoalemano

This is the most interesting $IREN theory I've read all week, and it's exactly what I said in my sequencing post: bad news first, good news after. Follow Frans's logic. It's sharper than it first looks. If you're planning to upgrade the board in 2027-2028, the sequencing almost writes itself. You pass the founder package FIRST, with the board that will approve it. Then you replace that board with a heavyweight, independent, cloud-and-AI-credentialed one, and the optics flip completely: The guys who voted for the grant are gone, the founders are secured and locked, and the new board exists precisely to keep them in check. It's the same playbook I just said. You don't drop the comp package at $100 alongside a deal, you drop it at the bottom, eat the hate for a week, and then let the good news arrive clean. Frans is just extending the sequence one step further: after the deals come the governance upgrades. The stick, then the carrot, then the crown. Institutions would love it. The grant is already baked into every model, it's a known, sealed number until FY2031. What isn't priced is a board built for a hyperscaler. That's pure upside on the governance line. And notice how this answers the two loudest criticisms at once. "Why now, why not with a deal?" Because you don't pass a founder package through a NEW board. You pass it through the old one, then upgrade. Bad news first, good news after. Sequencing, again. "The board has no cloud/AI experience" Correct, and the fair critics have been saying it for weeks. Which is exactly why a refresh would land so well: it's the one move that converts the sector's most-cited IREN weakness into a headline strength. The founders end up financially set for generations, chained to the ship until 2033, and answering to a harder, more qualified board than the one that paid them. Honestly? That's not a governance scandal. That's a governance ladder. To be clear, as Frans says himself: this is a theory. But if you want to be a hyperscaler, with the corporate machine and the brand to match, a matching board isn't optional. It's on the agenda somewhere. Watch the board seats. That's the tell now. Do your own research. This is not financial advice. I am long $IREN.

Frans Bakker D30.11K @FransBakker9812

Frans Bakker D30.11K @FransBakker9812What if $IREN is planning to alter the composition of their board of directors in 2027/2028, and this grant package needed to pass with the existing members of the board? Would it not be the ultimate show of governance to REPLACE the people that voted unanimously for this grant? On one hand, founders are set for life, no new board members can take that away from them. On the other hand, a new, highly qualified, experienced, and independent board, could be the ultimate demonstration of governance and compliance, going forward. Institutional investors would bake the current grants in their models, and be satisfied with a strong board that can keep the founders in check. Retail would see the guys leave that voted for this package. Founders will execute, and while having to deal with a more difficult board, be financially secure for multiple generations to come. I know this is just a theory, and most of you want to focus on the content of the package, but to me, it's much more a question of why, and why no

105 13 15.28K 閱讀原文 >釋出後IREN走勢看漲The IREN governance overhaul is seen as a strategic upgrade, and the author is bullish on its long-term prospects. - ChinoAleman D7.39K @chinoalemano

The $IREN Hunt #4: $CIFR. This chapter is different. And that difference is the point. The Hunt isn't a hit-piece series. It's an audit. And an audit that only ever finds villains isn't an audit, it's a script. So today: the peer that mostly passes. Cipher Mining. Bitcoin miner turned AI datacenter play, AWS and Fluidstack/Google leases, ~3.2 GW pipeline. The numbers, from the filings. CEO Tyler Page received: ~1.6% of the company in 2024 (a front-loaded year), ~0.75% in 2025. ~0.75% projected (more or less) for 2026. The full exec team: roughly 2.7%, then ~1.3%, stabilizing around ~1.3% a year, with Page consistently taking just under 60% of the exec pool. Credit where due. The Hunt is honest or it's nothing: ➟ The percentages DECLINE every year. ➟ Independent chair. ➟ Clawback policy. ➟ Anti-hedging. ➟ PSUs tied to market-cap hurdles. ➟ Moderate sizes, orthodox split. Of everything I've hunted so far, this is by far the most disciplined structure. NUAI and SLNH should take notes. Now, h

67 8 6.99K 閱讀原文 >釋出後IREN走勢極度看漲The equity and land ownership structure of IREN is superior to the problematic transaction of WULF; the author is bullish on IREN. - ChinoAleman D7.39K @chinoalemano

I see a lot of bad-faith actors around $IREN. And plenty of honest people simply misinformed BY those bad-faith actors. That's exactly why I'm running this Hunt Series, comparing IREN against names like $NUAI, $SLNH and $HUT, straight from the filings. IREN's comp package is among the best in the sector. The cleanest. The least predatory. Just some bad actors taking the headline out of proportion, taking 5 years of compensation to scare you. Now, some will say: "why not performance-based?" Fine. Let's play that movie forward. Dan and Will set a $70 stock price hurdle, and in exchange take 5% of the company. Then a $100 hurdle, another 5%. And so on, milestone after milestone, until they've carved out the whole thing. That's the HUT model. "But but but, make them set $300!" Sure. They'll set $1,000 just to please you. Come on. In the real world, boards set REACHABLE hurdles. That's the whole game. The exec hits the realistic target, collects 5% in one slice, and then? Then the stock price can go to hell for all they care. They already collected. Look at BITF. Awards that paid out with the stock at $6. Stock at $2 right after. They did everything (X post, etc etc) to get it to $6. Cash their bonus. And who cares about the stock price later. The bonus didn't fall with it. That's the dirty secret of "performance-based": it pays on the way up and doesn't claw back on the way down. Also, without performance, names like NUAI and SLNH hand out ~10% in a single year. Now compare IREN's structure. ~1% per year, for five years. FIXED share count, so it SHRINKS as a percentage every year the company grows. Locked for six years, they can't sell a single share on the way. Nothing more until fiscal 2031, in writing. They don't get paid for touching a price target once. They don't need to care to pump the stock. They get paid for still being there in 2033, with the entire ride, up or down, on their own backs. Is it the perfect package? No. The perfect package is 0%. Sure. Dreaming is free. In the real world, this is about as clean as this sector gets. The filings say so. The Hunt continues. This is not financial advice. Do your own research. I am long $IREN.

ChinoAleman D7.39K @chinoalemano

ChinoAleman D7.39K @chinoalemanoThe $IREN Hunt #3: $HUT. The series continues. Last hunt: $SLNH and its vest-on-exit chairman. Today, the biggest dollar figure in the entire space, and an award worth up to ~4-6% of the company. To one man. In one year. Hut 8. Bitcoin miner turned power-first AI infrastructure play. And home to one of the largest CEO pay packages in all of America. Straight from the proxy: CEO Asher Genoot's total 2025 compensation was $239,909,042. Not a typo. Two hundred forty million dollars. In one year. That's ahead of Broadcom's Hock Tan ($205M). Ahead of Blackstone's Schwarzman ($126M). A top-three pay package in the entire country, on a former Bitcoin miner. For context: his 2024 comp was $10.3M. A 23x jump in a single year. The driver: one-time "Transformation Awards" a mountain of PSUs granted in November 2025 to Genoot and his co-founder CSO Michael Ho. Run the percentage. At the grant-date fair value of ~$237M, against the share count and price at the time, that single award plausibly represents

126 16 16.65K 閱讀原文 >釋出後IREN走勢極度看漲The IREN compensation structure is more transparent than peers, and the author is bullish and already long.

126 16 16.65K 閱讀原文 >釋出後IREN走勢極度看漲The IREN compensation structure is more transparent than peers, and the author is bullish and already long.