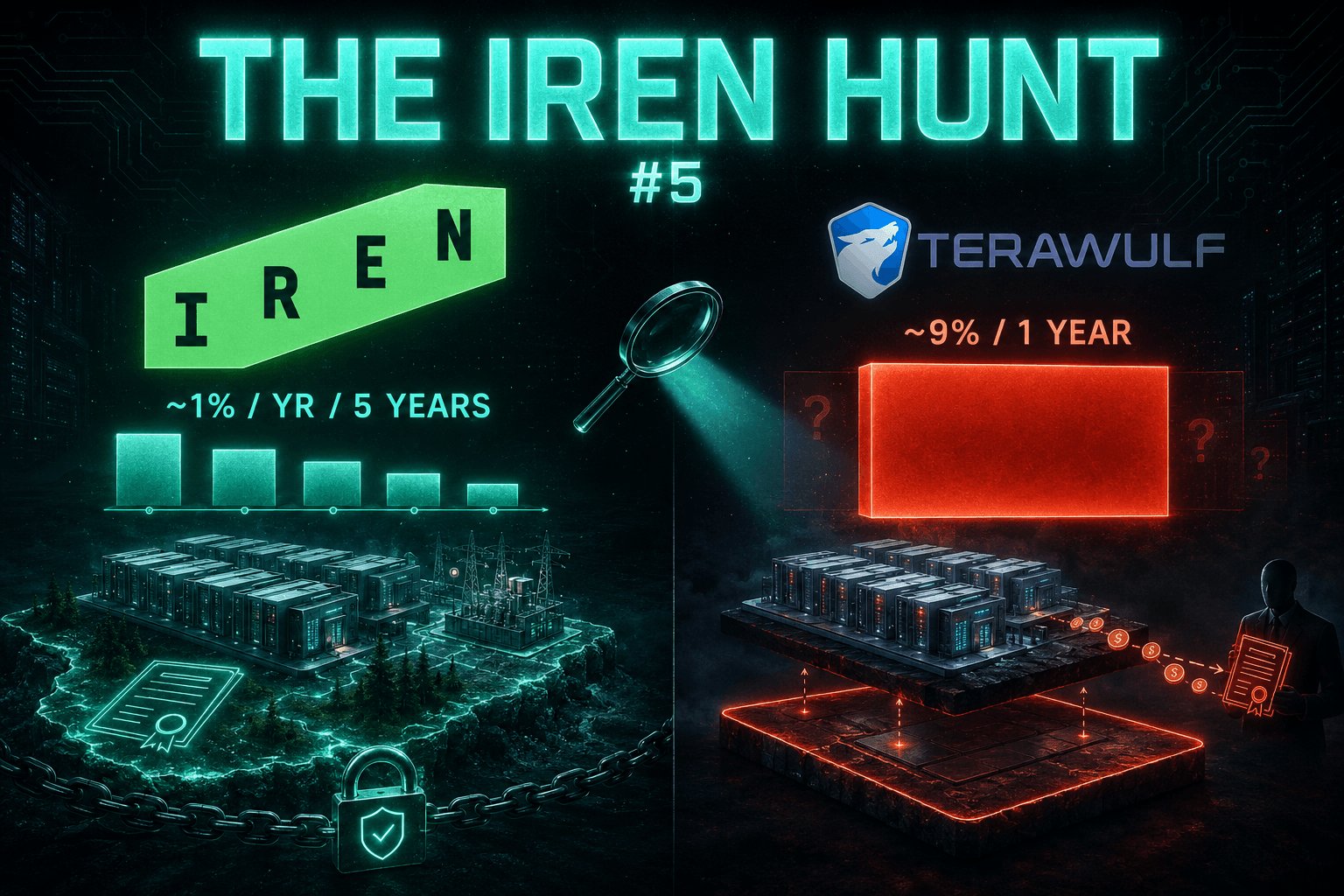

The $IREN Hunt #6: $WOLF.

No, not a typo.

Last hunt was $WULF, the datacenter landlord.

Today is WOLF, Wolfspeed, the silicon carbide semiconductor. Different sector, different story, and the darkest chapter of this series.

Because this one isn't about founder comp. It's about what dilution ACTUALLY means when things go wrong. Consider it the control experiment.

Wolfspeed filed Chapter 11 on June 30, 2025.

Prepackaged, 91 days, emerged September 29. Legally standard. Court-approved. Creditors first, that's the law of absolute priority.

No fraud, no hidden trick.

The 8-K said plainly the equity would be wiped.

Now what "wiped" means in numbers.

Old shareholders received 3 to 5 percent of the new company. An exchange ratio of roughly 0.0083.

Held 1,000 shares?

You got about 8.

The ticker stayed WOLF, so plenty of retail holders didn't even realize they no longer owned what they thought they owned.

And here's the part that belongs in this series: the reorganization plan reserved 10% of the NEW equity for the Management Incentive Plan, plus up to 5% more for long-term incentive plans.

Up to ~15% of the company, set aside for management.

Some of them are the ones who caused the current bankruptcy.

Not founders. Wolfspeed's founders left decades ago, this is the old Cree, founded 1987.

The reserved pool is for the team running it now, including a CEO who arrived in 2025, months before the filing. A team that put in no capital, reserved up to triple what the original owners were left holding.

To be fair, and the Hunt stays fair: reserved is not granted. The pool pays out over years, with vesting, typically tied to targets.

Creditors approved it because retention packages are standard in restructurings.

All of it legal, all of it disclosed.

Legal. Disclosed. And shareholders still ended with 8 shares per 1,000.

Now the lesson, because there is one.

X spent two weeks screaming about IREN handing its FOUNDERS ~5.1% over five years.

Founders who built it from zero, hold ~29M shares of their own, can't sell a single new share before 2029, and run a company with $2.2B in cash, positive net income, and Microsoft, NVIDIA and Dell on the customer list.

Meanwhile, in the real world, this is what an actual dilution event looks like: 99%+ real losses for holders, and up to 15% of the new company reserved for a management team that walked in the door last year.

The grant you're angry about is not the risk.

The balance sheet is the risk. Comp packages only matter if the company survives to pay them.

IREN's founders bet six locked years on survival and growth. Wolfspeed's shareholders learned what the alternative costs.

Choose your dilution.

Do you have any suggestions?

Drop it in the comments.

The Hunt continues.

Next ticker soon.

This is not financial advice. Do your own research.

I'm long $IREN.

TokenPulse BTC / 《海外の仮想通貨ニュースを最速で毎日お届け!》 Media Educator D19.79K @TokenPulseJP

TokenPulse BTC / 《海外の仮想通貨ニュースを最速で毎日お届け!》 Media Educator D19.79K @TokenPulseJP Cointelegraph Media Influencer D2.94M @Cointelegraph

Cointelegraph Media Influencer D2.94M @Cointelegraph

0 0 74 أصلي >اتجاه BTC بعد الإصدارهابط

0 0 74 أصلي >اتجاه BTC بعد الإصدارهابط Razz Shares Influencer Community_Lead B10.00K @Razzshares

Razz Shares Influencer Community_Lead B10.00K @Razzshares 5 5 64 أصلي >صاعد

5 5 64 أصلي >صاعد Bitcoin Takeover (BTCTKVR.com) Educator Media C4.16K @BTCTKVR

Bitcoin Takeover (BTCTKVR.com) Educator Media C4.16K @BTCTKVR 15 0 15.41K أصلي >اتجاه BTC بعد الإصدارمحايد

15 0 15.41K أصلي >اتجاه BTC بعد الإصدارمحايد 🐺 FREKI ANCIENT CRYPTO OG 2011 | HBAR XRP BTC FLR Influencer Media B10.75K @Freki_OG

🐺 FREKI ANCIENT CRYPTO OG 2011 | HBAR XRP BTC FLR Influencer Media B10.75K @Freki_OG $1 FLR☀️, Bullish Barbie Taylor D2.94K @BTtaylormade

$1 FLR☀️, Bullish Barbie Taylor D2.94K @BTtaylormade 7 1 106 أصلي >هابط بشدة

7 1 106 أصلي >هابط بشدة

LLY#1 Social mentions surged-

LLY#1 Social mentions surged- GIGGLE#2 Social mentions surged-

GIGGLE#2 Social mentions surged- MON#3 Social mentions surged-

MON#3 Social mentions surged- PENGU#4 Social mentions surged+101

PENGU#4 Social mentions surged+101 DOGS#5 Social mentions surged-

DOGS#5 Social mentions surged-